As the holiday season kicks off, many of us will be diving into shopping with an eye for bargains. Done well, it can make those expenses feel a little lighter. And the same goes for stock picking.

When it comes to equities, bargain hunting usually involves finding beaten-down stocks that remain fundamentally sound. They may have gotten caught up in a cyclical downturn – after all, there’s a reason the share price is down – but they aren’t necessarily bad portfolio options.

To uncover such opportunities, turning to Wall Street’s stock analysts can provide valuable insights. These experts have recently spotlighted two beaten-down stocks that could stage a comeback in 2025.

Using the TipRanks database, we’ve explored these two picks to understand why they might be poised for double-digit gains in the near future.

KinderCare Learning Companies (KLC)

The first stock on our beaten-down list is KinderCare, an early childhood education company that is part of the for-profit educational and child development sector. The firm was founded back in 1969 and is currently based out of Portland, Oregon; its network of educational centers extends across 40 states and is capable of serving up to 200,000 kids. This network includes some 1,500 branded early childhood education centers, and it is backed up by approximately 900 sites for before- and afterschool programs. The company also operates the line of Crème Schools, a premium early education network that offers parents and students engaged learning environments in a variety of themed classrooms. All in all, KinderCare has programs for children from the age of 6 weeks all the way up to 12 years.

While KinderCare has been in the early childhood education business for decades, the company only went public in October of this year. The KLC stock ticker entered the trading markets through an IPO that saw the company raise $576 million in gross proceeds. The offering closed on October 10 with shares priced at just over $28; since then, the stock has been falling – and it has lost 20% in November alone.

KLC’s share price decline has followed the earnings report from its competitor BFAM, which showed deceleration in both the quarterly revenue and the forward outlook. Also, the recent election results impacted KinderCare’s stock, particularly through the increased potential for some uncertainty given KLC’s significant exposure to government subsidies and the likelihood that the incoming Trump Administration will cut back on Federal spending. Finally, KLC’s first public earnings release came this month, and the company did not give further guidance for 4Q or FY25.

While the earnings release did not provide much in the way of guidance, it did beat the forecasts. The company reported Q3 revenue of $671.5 million, up 7.5% year-over-year and some $2 million better than had been expected. At the bottom line, KLC’s non-GAAP earnings came to 5 cents per share, where the Street had been expecting a 2-cent loss.

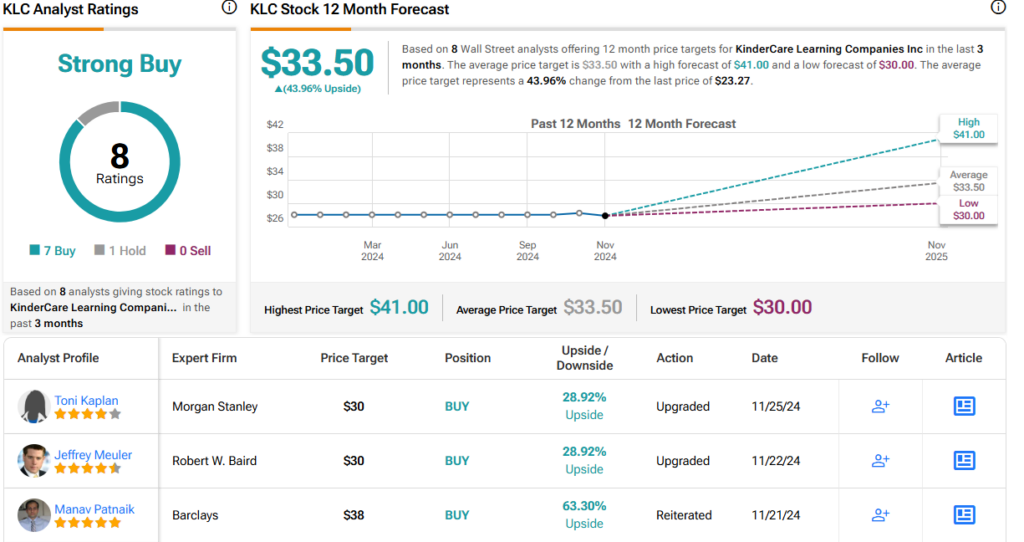

This stock has caught the eye of Morgan Stanley analyst Toni Kaplan, who notes that the recent slide opens up a buying opportunity. She writes of this new stock, “We see the recent decline in the share price as an attractive entry point… KLC’s ’25 EV/EBITDA multiple is now 3-turns below where it has been trading post-IPO… KLC currently also trades 2-turns below the average multiple of BFAM and LSD/MSD Business Services peers on ’25 EV/EBITDA. We find this move overdone, as not much has actually changed with regard to KLC’s fundamentals.”

Kaplan goes on to rate these shares as Overweight (i.e. Buy), an upgrade from Equal Weight. Her price target, set at $30, implies a one-year gain of 29%. (To watch Kaplan’s track record, click here)

Since entering the public markets, KLC stock has earned a Strong Buy consensus rating from the Street’s analysts, based on 8 reviews that include 7 Buys and 1 Hold. The shares are priced at $23.27 and their $33.50 average price target suggests that the stock will appreciate by 44% in the next 12 months. (See KLC stock forecast)

Roku(ROKU)

The next stock we’re looking at, Roku, is a leader in the field of on-demand streaming television. The company was a pioneer in its field, and today offers customers a subscription streaming experience that gives them the TV service they want, the way they want it. Customers can buy smart TVs with Roku’s capability built in or can purchase a Roku player to connect to an existing TV set; either way, the streaming service is purchased through a subscription contract.

The main difference between Roku and older cable services lies in user choice. Roku doesn’t bundle packages; rather, the company lets its customers choose what they want to watch. The internet-based service can support voice-activated controls for seeking programs, launching apps on the service, or even adjusting the volume. Roku’s product line includes the eponymous player, the company’s smart TV, audio speakers, and accessory remotes for the TV or even for smart home functionality.

From the user perspective, Roku requires an internet connection – but it will then provide access to a large range of streaming apps as well as the usual broadcast TV channels or even satellite or cable channels. Roku brings the flexibility of the internet to the world of TV.

That said, shares in Roku are down this year. The stock has fallen just over 26% in the year-to-date. Recent headwinds include a reduced guide for fourth-quarter sales growth on its platform segment, with the company dropping it from 15% y/y to 14%. In addition, the company suggested that it will stop reporting certain business metrics next year, causing some concern that it will reduce its financial transparency. The Trade Desk also recently announcing a new streaming operating system has further dampened sentiment.

Despite the worries, the company did report generally sound results for 3Q24. The company’s top line, of $1.06 billion in revenues, was up more than 16% year-over-year and beat the forecast by $40 million. Roku ran a net loss in the quarter, of 6 cents per share, but that represented a solid year-over-year turnaround from the $2.33 net EPS loss recorded in 3Q23 – and it was 27 cents per share better than had been anticipated.

For Baird analyst Vikram Kesavabhotla, the key point to understanding Roku is threefold. Explaining his stance, he writes, “Historically, we have been hesitant regarding the company’s execution in a rapidly evolving streaming landscape – but we now think shares are overlooking the meaningful changes in the business and the attractive long-term opportunity. In particular, our optimism is predicated on: 1) increasingly favorable industry trends, 2) positive developments in the strategy, and 3) encouraging early indicators in recent results. Investor expectations seem better calibrated post-3Q – and from here, we see potential upside to estimates/valuation over time.”

These comments back up Kesavabhotla’s Outperform (i.e. Buy) rating and his price target of $90 points toward a potential one-year upside of 33%. (To watch Kesavabhotla’s track record, click here)

There are 21 recent reviews on record for ROKU shares, and they break down to 9 Buys, 10 Holds, and 2 Sells for a Moderate Buy consensus rating. The stock is selling for $67.71 and has an average price target of $79.78, suggesting an upside of 18% on the one-year time horizon. (See Roku’s stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Kaitlin Rogers is a writer, editor, and news junkie. She has been working in the media industry for over five years, and her work has appeared in dozens of publications.

Kaitlin graduated from Michigan State University with a bachelor's degree in journalism and political science.