(Bloomberg) — It was little more than two and a half years ago that Franklin Templeton’s (BEN) boss Jenny Johnson took to LinkedIn to express her excitement about buying European private credit stalwart Alcentra. Today, a key part of the acquired business is struggling to justify the enthusiasm.

Most Read from Bloomberg

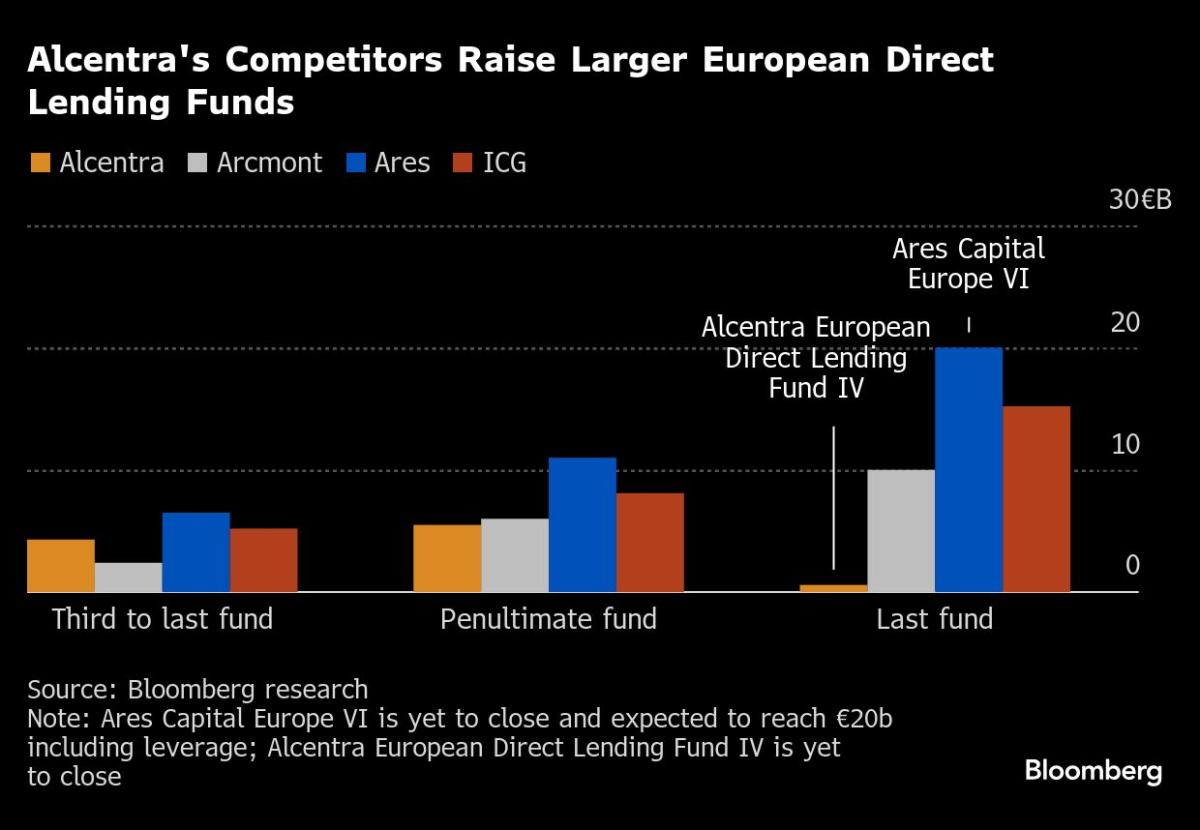

In its heyday, Alcentra was up there with current direct-lending success stories such as Ares Management Corp. and Intermediate Capital Group Plc. as they jousted for preeminence in making loans to Europe’s companies. But unlike old rivals that are expanding their assets at breakneck speed, Alcentra has shrunk.

At its peak it managed about $43 billion of assets, according to Fitch Ratings. By the time Franklin struck the deal to acquire the London-based lender, it had $38 billion. It now has about $32 billion. Alcentra’s corporate direct-lending franchise, the engine room of most private credit businesses, has halved from €12 billion ($12.7 billion) in 2020 to €6 billion, according to an analysis by Bloomberg News of the firm’s public filings.

With other asset-management giants such as BlackRock Inc. (BLK) and State Street Corp. (STT) shopping around for their own purchases in the booming $1.6 trillion private credit market, Alcentra is a cautionary tale from the industry.

Franklin’s purchase of Alcentra in 2022 is dwarfed by BlackRock’s acquisition of HPS Investment Partners — and the low sale price reflects problems that predate the sale — but its ongoing troubles with its once-flagship fund are a reminder that fortunes can change fast in this industry.

Back in 2019 Alcentra raised one of Europe’s then largest direct-lending funds. Botched leadership changes, a staff exodus and some poor investments have weighed heavily. Five years on it’s still trying to raise a follow-on fund.

An Alcentra spokesperson says the firm’s overall assets under management have been “stable” since Franklin’s takeover was completed in November 2022, and that it has seen “strong momentum and performance” in other parts of the business: “Over the last 12 months, we’ve seen successful fund closes and significant fundraising traction in our structured credit and special situations vintages, as well as inflows into our European liquid credit strategies.”

Nevertheless, the travails of its direct-lending fund carry a warning for the private credit asset class more broadly. Funds that can’t keep up with returns offered by peers, or who lose staff, are finding it hard to bring in new money as unforgiving investors increasingly put their faith in the promised stability of private capital’s biggest beasts.

“More firms have issues now that were previously not apparent,” says Andrew Bellis, head of private debt at Partners Group, speaking generally about the market rather than Alcentra. “There will be a shakeout in the industry, but that happens over a long period of time. We might look back and say, ‘What happened to that firm that used to be big?’”

First-Mover Advantage

Alcentra was an early mover into European direct lending along with fellow pioneers Ares, ICG and Arcmont Asset Management. But even as this industry has flourished — as private firms muscle in on the lucrative corporate loan business once dominated by Wall Street — the trailblazer has floundered.

While rivals have been targeting fundraisings comfortably over €10 billion and expanding their direct-lending arms, Alcentra is the odd one out. Its latest fund for this market was registered in Luxembourg more than four years ago and, so far, there’s been no public statement about it reaching any milestones.

Franklin’s acquisition was part of a major expansion in alternative assets by the $1.6 trillion investment giant after buying Lexington Partners, a private equity fund manager. Franklin and its ilk have been drawn to private markets by the allure of higher returns and as a way to win back clients who’ve shunned more traditional actively-managed stock and bond funds.

Franklin has been one of the asset managers most affected by outflows in recent years, with clients pulling about $176 billion from its funds since 2019, according to Morningstar Inc. It’s also dealing with the fallout of another, more traditional acquisition. Ken Leech, the former star trader of Western Asset Management Co., which Franklin bought through its acquisition of Legg Mason, has been charged by the US for alleged fraud.

“Franklin Templeton manages $250 billion in alternative assets, and the Alcentra business is an important part of our offering in the alternative credit space,” a spokesperson for the company says.

Part of the problem for Alcentra’s direct-lending arm has been performance. The fund manager has been involved in several debt-for-equity swaps since 2019, according to Bloomberg research, a sign that things weren’t going well for these companies. These include Lifetime Training, an apprenticeship training provider that struggled to recover from the Covid-19 pandemic, and Caroola (previously known as Optionis), a professional services provider that was crippled by a cyber hack in 2022, according to public filings.

One Alcentra investor, Strathclyde Pension Fund, said at a recent meeting that the lender provided a 6.7% return over the last year, according to documents seen by Bloomberg, while two other private-debt investments, Barings and Partners Group, delivered 10.9% and 11.1%. Since the start of Strathclyde’s investment, however, Alcentra does stack up well against its peers.

Strathclyde was candid about where some of the more recent issues arose: “Alcentra has suffered from a high level of senior turnover and has had a change of ownership.” The pension fund has decided to run off its investment, according to the documents, meaning it won’t put any more money in.

“The one thing you want to see is consistency in deal performance and the team,” says Vasileios Kocheilas, a seasoned investor in private credit funds. “Investing is about finding the right people to do the right things.”

As smaller private credit firms find it tougher to deliver that consistency, and to get new fundraising off the ground, private-capital behemoths such as Blackstone Inc. (BX) and Ares are taking the lion’s share of the market’s growth. Investors, known as limited partners, are voting with their feet.

“LPs have to make tough decisions on which managers to back,” says Mike Dennis, partner and co-head of European credit at Ares, speaking generally about the market. “We’re seeing LPs consolidate their manager relationships because of liquidity constraints. And for some of those small managers, it’s very difficult to say what their differentiation is.”

Size isn’t everything, however. Some of the old titans of traditional money management haven’t cracked this red-hot asset class. Fidelity International halted its early European direct-lending activities this year. BlackRock will hope that buying a premium outfit like HPS will spare any pain, even if it isn’t cheap.

At the less exalted end of the private credit market, some are bracing for the emergence of zombie funds, so-called because they own a bunch of illiquid assets and are struggling to raise cash to buy more. Instead, they begin a slow process of withering away. It’s a familiar sight in private equity, where hundreds of firms are in that unhappy position.

In private credit, the assets are loans with fixed maturities — so, unlike equity, a fund can’t stumble on forever. But a firm’s future is predicated on its ability to raise more capital and keep scaling. As this nascent asset class matures, subpar performance may lead to a sticky end.

“We’re going to see more zombie funds as credit managers will have had so many problematic deals that no one will be willing to give them any more money,” Kocheilas concludes.

Kaitlin Rogers is a writer, editor, and news junkie. She has been working in the media industry for over five years, and her work has appeared in dozens of publications.

Kaitlin graduated from Michigan State University with a bachelor's degree in journalism and political science.