(Bloomberg) — Bond traders have rarely suffered so much from a Federal Reserve easing cycle. Now they fear 2025 threatens more of the same.

Most Read from Bloomberg

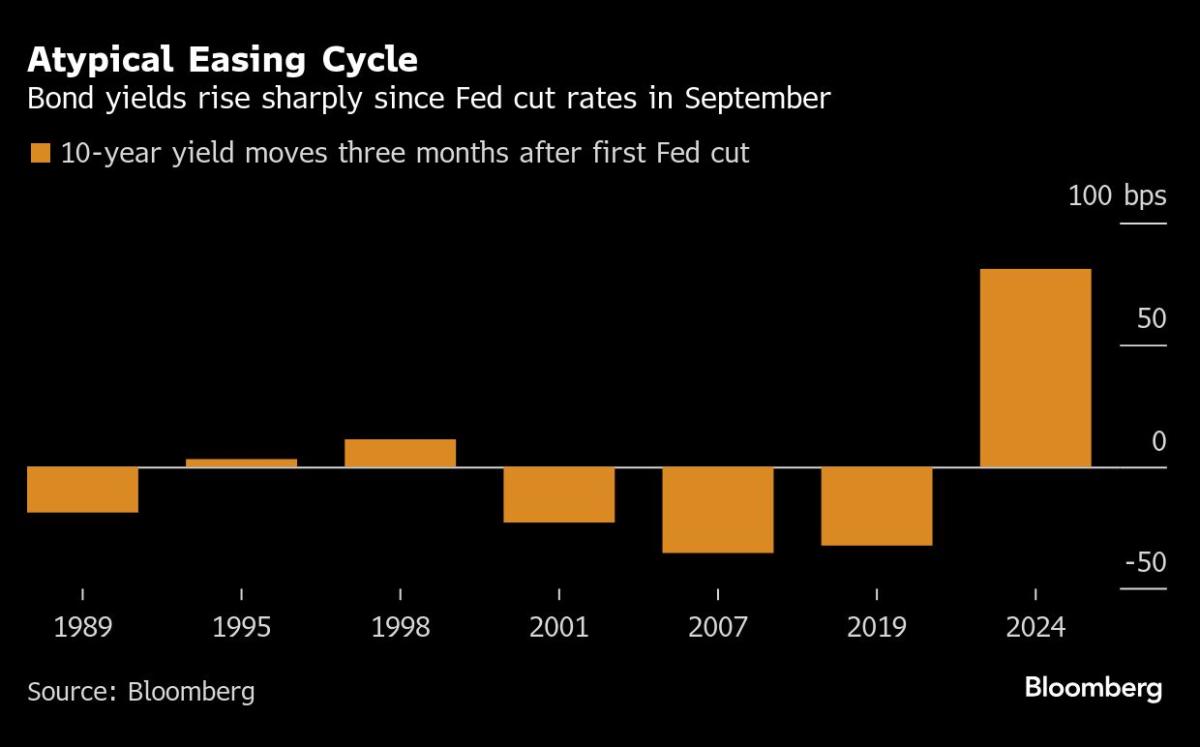

US 10-year yields have climbed more than three-quarters of a percentage point since central bankers started slashing benchmark interest rates in September. It’s a counterintuitive, loss-inducing response, marking the biggest jump in the first three months of a rate-cutting cycle since 1989.

Last week, even as the Fed delivered a third consecutive rate cut, 10-year Treasury yields surged to a seven-month high after policymakers led by Chair Jerome Powell signaled that they are prepared to slow the pace of monetary easing considerably next year.

“Treasuries repriced to the notion of higher for longer and a more hawkish Fed,” said Sean Simko, global head of fixed-income portfolio management at SEI Investments Co. He sees the trend continuing, led by higher long-term yields.

Rising yields underscore how unique this economic and monetary cycle has been. Despite elevated borrowing costs, a resilient economy has kept inflation stubbornly above the Fed’s target, forcing traders to unwind bets for aggressive cuts and abandon hopes for a broad-based rally in bonds. After a year of sharp ups and downs, traders are now staring down another year of disappointment, with Treasuries as a whole barely breaking even.

The good news is that a popular strategy that has worked well during past easing cycles has gained renewed momentum. The trade, known as a curve steepener, is a wager that Fed-sensitive short-term Treasuries would outperform their longer-term counterparts — which they generally have of late.

‘Pause Phase’

Otherwise, the outlook is challenging. Not only do bond investors have to contend with a Fed that is likely to stay put for some time, they also face potential turbulence from the incoming administration of President-elect Donald Trump, who has vowed to reshape the economy through policies from trade to immigration that many experts see as inflationary.

“The Fed has entered a new phase of monetary policy — the pause phase,” said Jack McIntyre, portfolio manager at Brandywine Global Investment Management. “The longer it persists, the more likely the markets will have to equally price a rate hike versus a rate cut. Policy uncertainty will make for more volatile financial markets in 2025.”

What Bloomberg strategists Say …

The last Federal Reserve meeting of the year is in the rear view and its results are likely to support curve steepeners into the turn of the year. Though once Donald Trump’s administration takes the helm in January, that dynamic has scope to stall amid uncertainties surrounding the government’s new policies.

—Alyce Andres Read more on MLIV

Bond traders were caught off guard last week after Fed policymakers signaled greater caution over how quickly they can continue reducing borrowing costs amid persistent inflation concerns. Fed officials penciled in only two quarter-point cuts in 2025, after bringing interest rates down by a full percentage point from a two-decade high. Fifteen of 19 Fed officials see upside risks to inflation, compared with just three in September.

Traders quickly recalibrated their rate expectations. Interest-rate swaps showed that traders haven’t fully priced in another cut until June. They are betting a total reduction of about 0.37 percentage point next year, less than the half-point median projection on the Fed’s so-called dot-plot. In the options market, though, trade flows have skewed toward a more dovish policy path.

Bloomberg’s benchmark for Treasuries fell for a second week, all but wiping out this year’s gain, with long-dated bonds leading the selloff. Since the Fed began cutting rates in September, US government debt has declined 3.6%. In comparison, bonds had positive returns in the first three months of each of the past six easing cycles.

The recent declines in long-term bonds haven’t attracted many bargain hunters. While strategists at JPMorgan Chase & Co., led by Jay Barry, recommended clients buy two-year notes, they said they don’t “feel compelled” to purchase longer-maturity debt, citing the lack of key economic data in the weeks ahead and thinner trading into year-end, as well as fresh supply. The Treasury is slated to auction $183 billion of securities in the days ahead.

The current environment has created the perfect conditions for the steepener strategy. US 10-year yields traded a quarter-point above those on two-year Treasuries at one point last week, marking the biggest gap since 2022. The differential narrowed somewhat Friday after data showed the Fed’s preferred measure of inflation advanced last month at the slowest pace since May. But the trade is still a winner.

It’s easy to understand the logic behind this strategy. Investors start to see value in the so-called short end because, at 4.3%, yields on two-year notes are almost on par with three-month Treasury bills, a cash equivalent. But two-year notes have the added advantage of potential price appreciation if the Fed cuts rates more than expected. They also offer value from a cross-asset standpoint, given US stocks’ stretched valuations.

“The market views bonds as cheap, certainly relative to stocks, and see them as representing insurance against an economic slowdown,” said Michael de Pass, global head of rates trading at Citadel Securities. “The question is, how much do you have to pay for that insurance? If you look at the very front end now, you’re not having to pay a ton.”

In contrast, longer-term bonds are struggling to entice buyers amid sticky inflation and a still robust economy. Some investors are also wary of Trump’s policy platform and its potential not only to fuel growth and inflation, but also to worsen an already large budget deficit.

“When you start to factor in the president-elect Trump administration and spending — that certainly can and will push those longer-term yields higher,” said Michael Hunstad, deputy Chief Investment Officer at Northern Trust Asset Management, which oversees $1.3 trillion.

Hunstad said he favors inflation-linked bonds as a “pretty cheap insurance” against rising consumer prices.

What to Watch

Economic data:

Dec. 20: University of Michigan consumer confidence survey (final); Kansas City Fed services activity

Dec. 23: Chicago Fed National Activity Index; Conference Board Consumer Confidence

Dec. 24: Building Permits; Philadelphia Fed non-manufacturing activity; Durable goods; New home sales; Richmond Fed manufacturing index and business conditions

Kaitlin Rogers is a writer, editor, and news junkie. She has been working in the media industry for over five years, and her work has appeared in dozens of publications.

Kaitlin graduated from Michigan State University with a bachelor's degree in journalism and political science.