Kinder Morgan (NYSE: KMI) offers investors a big-time income stream. The natural gas pipeline giant currently yields 6.4%, which is one of the highest payouts in the S&P 500 (where the average is 1.4%). Despite its high yield, Kinder Morgan offers one of the safest income streams in that broad market index.

The safety of its payout was evident in its first-quarter report. Here’s a look at those numbers and why they put the pipeline stock’s big-time dividend on a rock-solid foundation.

As steady as it goes

Kinder Morgan produced $1.4 billion, or $0.64 per share, of distributable cash flow (DCF) during the first quarter. DCF was up 5% from last year on a per-share basis.

It easily covered the company’s high-yielding dividend, which it recently raised by about 2% to $0.2875 per share each quarter ($1.15 annualized). That marked the company’s seventh straight year of increasing its dividend.

The pipeline company continues to produce very stable and growing cash flow. Roughly 68% of its earnings come from take-or-pay and hedging contracts, which lock in its revenue. Most of its remaining earnings come from long-term, fee-based contracts, limiting its exposure to commodity price volatility.

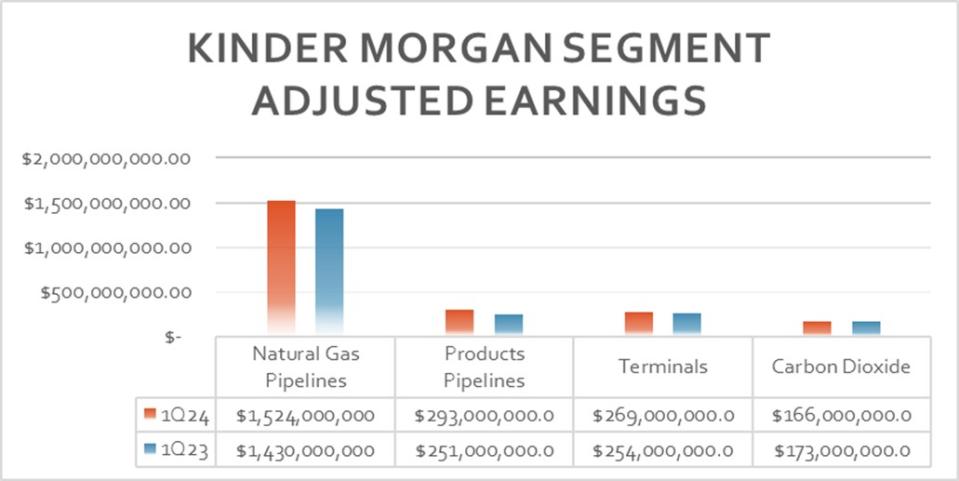

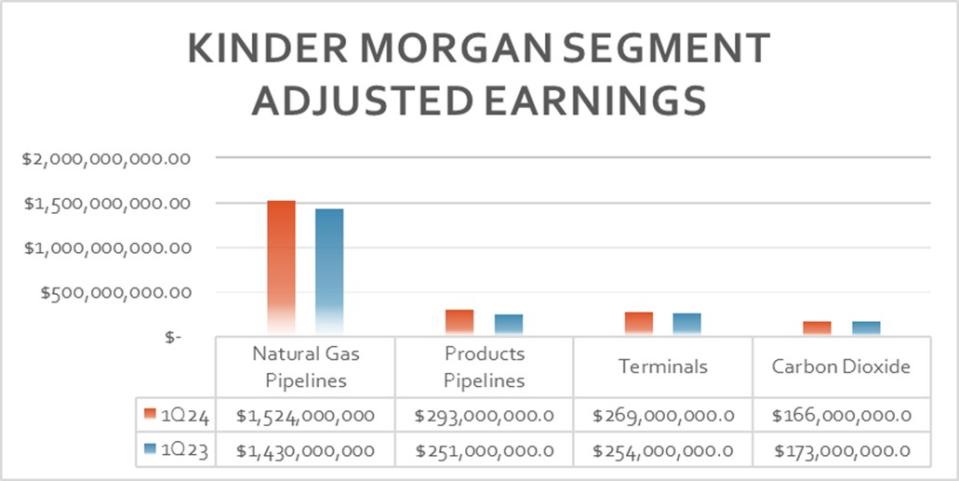

Meanwhile, its stable cash-flow sources are growing as the company expands its operations. Kinder Morgan delivered earnings growth across 3 of its 4 operating segments in the first quarter:

Earnings in the company’s core natural gas pipeline business rose 7% year over year. Fueling that improvement was higher margins from its storage assets, higher volumes from its gathering systems, and the acquisition of STX Midstream.

Kinder Morgan’s products pipeline operations had a standout quarter, with earnings surging 17%. The company benefited from higher rates on existing assets and contributions from recently completed capital projects. Finally, earnings from its terminals rose 6%, driven by liquids terminals expansion projects and higher rates on its Jones Act terminals.

The earnings growth from those three segments more than offset the 4% earnings decline from its carbon dioxide business. The main drag was lower carbon dioxide sales volumes. Commodity price movements largely offset each other. Likewise, lower crude oil volumes offset higher natural gas liquids output.

Kinder Morgan produced nearly $1.2 billion in cash flow from operations during the first quarter. It paid out about half that money in dividends ($631 million) and used about half to fund capital expenses ($619 million). That left it with a slight shortfall ($61 million) that it easily covered with its strong balance sheet.

Kinder Morgan ended the period with a 4.1x leverage ratio, well within its 3.5x-4.5x target range. That supported the company’s investment-grade credit rating.

On track for another solid year

Kinder Morgan’s solid showing in the first quarter kept it on track to achieve its full-year guidance forecast. The natural gas pipeline company expects to produce about $5 billion, or $2.26 per share of DCF. That would put its dividend payout ratio at around 51% this year, which is very conservative for a company producing such stable cash flow.

As a result, it should generate a little less than $2.5 billion in excess free cash flow that it can use to fund capital projects and maintain its strong financial flexibility. It expects capital spending to be at the upper end of its $1 billion-$2 billion annual range in the near term.

The company ended the first quarter with $3.3 billion of committed capital projects in its backlog, an increase from $3 billion at the end of last year. Kinder Morgan continues to find high-return expansion projects, with the bulk (80%) focused on lower-carbon energy like natural gas, renewable natural gas, and renewable fuels.

The midstream company’s growing earnings and projected excess free cash flow drive its view that it will end this year with a 3.9x leverage ratio. That gives it additional financial flexibility to make opportunistic acquisitions or share repurchases.

An extremely solid dividend stock

Kinder Morgan generates very durable cash flow that steadily rises. That enables the pipeline company to pay an attractive dividend, invest in its continued expansion, and maintain a strong balance sheet. Those features put its big-time payout on a firm foundation, making Kinder Morgan an excellent option for those seeking to collect a steadily rising passive-income stream.

Should you invest $1,000 in Kinder Morgan right now?

Before you buy stock in Kinder Morgan, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Kinder Morgan wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $514,887!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of April 15, 2024

Matt DiLallo has positions in Kinder Morgan. The Motley Fool has positions in and recommends Kinder Morgan. The Motley Fool has a disclosure policy.

This 6.4%-Yielding Dividend Stock Remains an Extremely Safe Option for Passive Income was originally published by The Motley Fool