It has been nearly four years since C3.ai(NYSE: AI) went public, and a look at the company’s performance on the stock market since its initial public offering (IPO) doesn’t paint a pretty picture. Its shares have lost 72% of their value since then.

The stock did enjoy a spike in the first half of 2023 when the hype around artificial intelligence (AI) technology was gaining steam, but even those gains have faded. Even 2024 has unfolded in a similar manner for C3.ai investors; after a bright start, the stock lost its momentum and is down 8% this year. That’s in stark contrast to fellow AI software specialist Palantir Technologies, which has witnessed a 162% surge in its stock price this year thanks to the growing demand for its AI software platforms.

Start Your Mornings Smarter! Wake up with Breakfast news in your inbox every market day. Sign Up For Free »

But can C3.ai turn its fortunes around and become a solid investment over the next five years? Let’s find out.

The demand for AI software platforms is expected to grow at an incredible annual rate of almost 41% over the next five years, according to market research firm IDC. More specifically, the size of this market is expected to jump to $153 billion in 2028 as compared to just $28 billion last year. So, the possibility of a turnaround in C3.ai’s fortunes cannot be ruled out considering that the market it serves is currently in the early phases of its growth.

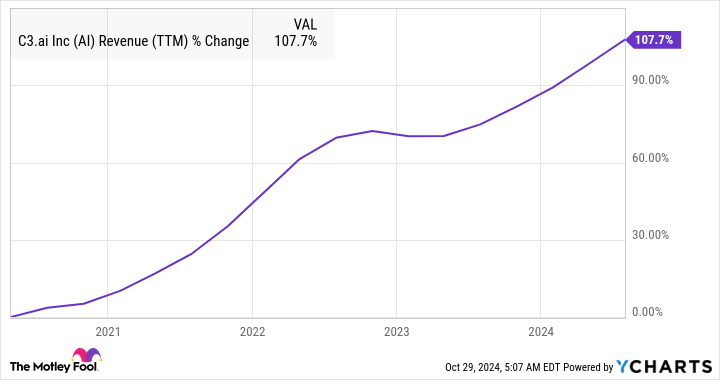

It is worth noting that the stock’s underperformance in recent years is the result of a change in its business model from a subscription-based service to a consumption-oriented one. C3.ai made this change in August 2022, which was the beginning of the second quarter of its fiscal year 2023. As the following chart tells us, the company’s growth took a hit following the change of business model in the second half of 2022.

AI Revenue (TTM) Chart

C3.ai management pointed out at that time that it would take nearly seven quarters for the change of business model to scale up and help the company achieve the revenue growth levels that it was achieving before the transition. The company seems to be walking the talk.

C3.ai released its fiscal 2025 first-quarter results (for the three months ended July 31) in September this year. This was the eighth quarter since the company announced the business model change, and the company reported a 21% year-over-year increase in revenue to $87.2 million. That was an improvement over the 16% revenue growth that the company clocked in fiscal 2024 to $310.6 million.

C3.ai’s fiscal 2025 revenue forecast of $370 million to $395 million indicates that its top line could increase by 23% on a year-over-year basis at the midpoint. That points toward an improvement in C3.ai’s growth rate this year, suggesting that the company’s business model change is indeed working.

One reason why that may be the case is that the switch to a consumption-based model means that C3.ai has lowered the entry barrier for customers looking to deploy generative AI applications. Earlier, C3.ai customers would have had to enter into subscription contracts for a certain period of time, which would have required the two parties to enter into negotiations.

But that’s not the case anymore. Now under the pay-as-you-go model, customers simply need to pay for the services they use. This reduced friction explains why there has been a significant increase in the number of pilot projects that C3.ai is currently engaged in. In the first quarter of fiscal 2025, C3.ai was engaged in a total of 52 pilot projects as compared to 24 in the same quarter last year.

At the same time, there has been a considerable increase in the number of deals that the company has been signing of late. C3.ai struck a total of 71 deals in the first quarter of fiscal 2025, up from just 32 in the same quarter last year. Another thing worth noting here is that the company is now getting a nice chunk of its deals from federal agencies.

Management pointed out on the September earnings conference call that the company entered into “new expansion agreements with the United States Air Force, the U.S. Navy, U.S. Marine Corps, and the U.S. Intelligence Community among others.” Moreover, the company is now getting more than 30% of its bookings from federal agencies, suggesting that it is gaining influence in this potentially lucrative market where Palantir has been the dominant player so far.

Analysts are understandably upbeat about C3.ai growth prospects going forward, expecting its revenue to increase in a healthy double-digit range over the next couple of years.

AI Revenue Estimates for Current Fiscal Year Chart

At the same time, C3.ai’s unit economics seem to be turning favorable as well. That’s evident from the fact that its revenue is increasing at a faster pace than its expenses, as seen in the chart below.

AI Total Expenses (Quarterly) Chart

The chart also tells us that C3.ai’s expenses are coming down, which bodes well for its bottom-line performance in the long run.

A combination of healthy revenue growth along with an improving cost profile should help C3.ai become profitable in the long run. Analysts are expecting the company to post an adjusted loss of $0.54 per share in the current fiscal year. However, that number is expected to shrink in the next fiscal year.

AI EPS Estimates for Current Fiscal Year Chart

More importantly, C3.ai is expected to attain non-GAAP profitability in a couple of fiscal years, as seen in the chart above. Even better, analysts are expecting C3.ai’s bottom line to improve at an annual rate of almost 51% for the next five years. That’s impressive considering that competitor Palantir’s earnings are projected to increase at a compound annual rate of 57% for the next five years.

However, the big difference between these two AI stocks is the valuation. While C3.ai is trading at 9.4 times sales, Palantir has a very rich price-to-sales ratio of 43.

C3.ai could therefore be a solid bet for investors considering the acceleration in its growth, a relatively attractive valuation, and its ability to deliver robust growth in its earnings. The combination of these factors could help the stock overcome its disappointing performance and deliver attractive gains over the next five years.

Before you buy stock in C3.ai, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and C3.ai wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $829,746!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of October 28, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Palantir Technologies. The Motley Fool recommends C3.ai. The Motley Fool has a disclosure policy.

Where Will C3.ai Stock Be in 5 Years? was originally published by The Motley Fool

Kaitlin Rogers is a writer, editor, and news junkie. She has been working in the media industry for over five years, and her work has appeared in dozens of publications.

Kaitlin graduated from Michigan State University with a bachelor's degree in journalism and political science.